07.09.2019

The 10 Key Steps of Mergers and Acquisitions in How to Sell a Company

Por

Furió Párraga, Ascensión

Por

Furió Párraga, Ascensión Process and Timetable

Mergers and Acquisitions is a legal practice which is closely related with the sale and acquisition of a company. M&A is a process of purchasing and/ or joining of another company or corporate assets. The abbreviation M&A is commonly known to law firms, financial advisors, banks and companies, who are responsible for the buying or selling companies or business commerce. Therefore, it is a common abbreviation and process, known in any country around the world. Despite it being standard process, it is necessary to know how it is usually carried out. M&A has its own language, terms, customs, trends and ultimately key steps.

Below, we will explain the key steps to entirely understand the dynamics and process of an acquisition transaction.

Process

The M&A process has been linked to being both a growth strategy and part of the financial institution in a favourable economic environment because all M&A negotiations require a number of commitments. It is essential to understand which party (seller or buyer) wants more in the negotiations. If you do not clarify who is who, believe us, you will lose.

Who wants the deal more, the buyer or the seller? Are there several interested parties competing against each other? Can you negotiate key conditions without increasing the price? Is the price of the deal attractive enough that the seller is willing to take subsequent indemnity risks that are higher than they would have preferred? Are you being advised by a M&A expert who knows why certain issues are not worth fighting for?

It is important that your M&A advisory team establishes a relationship with the buyer’s lawyers (the other party) and never allows the negotiations to heat up or become antagonistic. All negotiations must be conducted with courtesy and professionalism.

Estimated Closing Timetable

After many years of advising transactions, there is only one undoubtable conclusion:

- The estimated time of completing a transaction is always longer in reality. A deal is never completed in the initial scheduled time.

- Whatever transaction, however simple, always ends up complicated. Do not waste energy in trying to win a losing battle.

- There is no deal without dawn, it almost always ends on a long and absurd night that lasts until the early hours.

The Letter of Intent (LOI) (Non-Binding Indicative Offer) is critical

One of the biggest mistakes made by the sellers is to not properly negotiate the letter of intent. The letter of intent is anything but “just intentions.” The letter of intent will be the backbone of the process. Although a non-binding document (which may be binding), we all know that the letter of intent represents much more than just a letter of intent.

Frequently, a buyer will present the seller with a non-binding letter of intent or a term sheet that lacks details about the key terms of the transaction. If the buyer is a company of a certain volume or one that has experience in acquiring other companies, it will give the impression to the seller that these preliminary documents are rather an internal formality of their process and, therefore must be signed quickly so that the buyer can move on without delay to the “most important” stages of the acquisition process (such as due diligence and the negotiation of final acquisition documents).

However, the seller’s bargaining power is the greatest at the time just before signing a letter of intent or a term sheet. These documents, whilst not binding on trading conditions, are extremely important to ensure the likelihood of a favourable agreement for the seller. Once the letter of intent or term sheet is signed, the buyer’s period of inactivity is opened thanks to the letter of intent.

This is the case, particularly, when the buyer has required an exclusivity clause prohibiting the seller from talking to other potential buyers for a specified period of time during which the final sale agreement must be closed.

To avoid this trap, the seller needs to negotiate the terms of the letter of intent or term sheet, with the help of its legal and financial advisors, as if it were a binding document.

The key terms to negotiate in the letter of intent or term sheet are as follows:

- The price, if it will be paid in cash and when, or if part of the purchase price is deferred or postponed.

- Any adjustment to the price and how these adjustments will be calculated.

- The extent and the duration of any exclusivity or non-sale clause (as short as possible, for example, 15 to 30 days)

- The binding or non-binding nature of other terms (except with regard to confidentiality and exclusivity).

- Extent of the compensation and whether or not the buyer will subscribe an insurance policy to cover the declarations and guarantees against the damages resulting from a falsehood or non-compliance derived from them.

- The amount and duration of any price retention or the establishment of an unavailable deposit or escrow agreement given in guarantee of potential compensation.

Trading and Closing a M&A trade

Most M&A trades can go on for a long period of time from when conversations start until the transaction is completed.

Normally, the process takes between 4 to 6 months. The period will depend on the urgency of the buyer to carry out Due Diligence and complete the transaction, and whether the selling company is able to complete the competitive process of selling a company, whilst generating interest from multiple companies. However, there are several inputs that can be made to shorten this period:

- The seller must collect all key contracts, corporate records, financial statements, patents and any other necessary information and make these available to the potential buyer (either via conference call or face to face meeting).

- With the help of a private equity company or financial advisor, a strictly controlled auction sale process can be carried out. That way potential buyers are forced to make decisions in a shorter time frame and in a competitive environment.

- A lead negotiator should be appointed by the seller, who has experience in M&A operations and can make quick decisions on behalf of the company.

- The CEO of the company must be prepared to explain the added value that the seller will provide to the buyer.

- The company’s financial advisor should be prepared to answer any financial question and to defend the predicted financial projections.

- The M&A advisor should be asked to identify and assist on how to resolve possible delays due to regulatory requirements (competence, Regulatory Authorities, etc.) and contractual approval and other third-party rights.

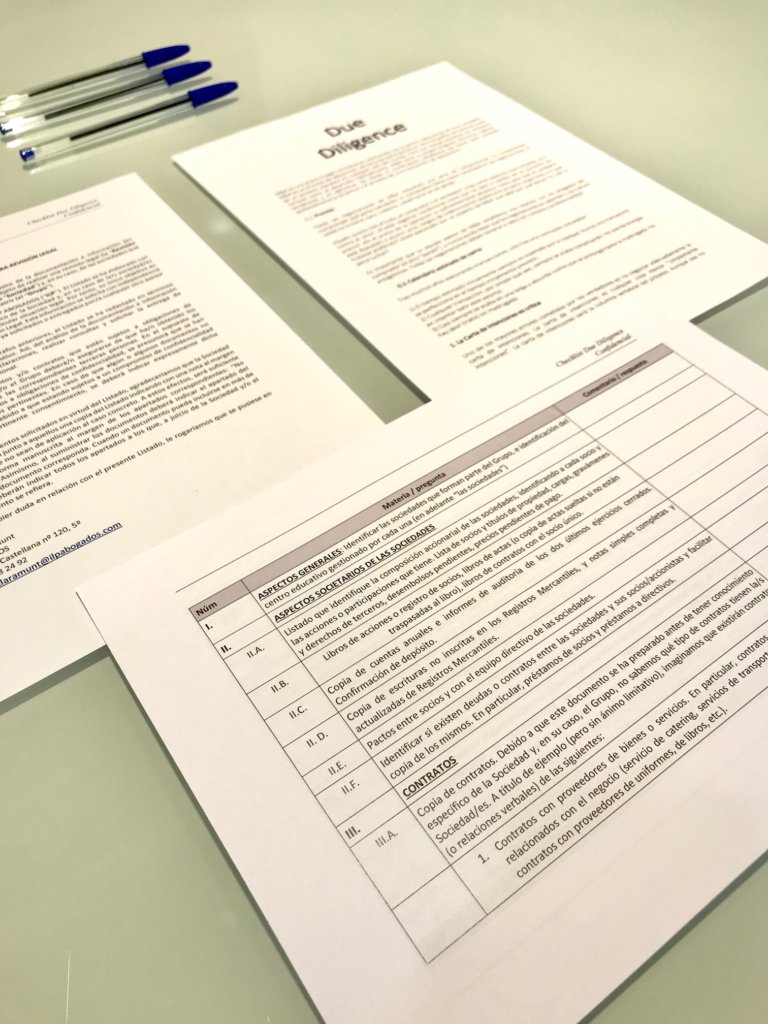

Due Diligence

The transactions of M&A involve the buyer thoroughly examining all the relevant information of a company that they want to acquire. Before committing to the deal, the buyer will want to make sure that they know what they are buying and what obligations they will take over. Additionally, they will want to know the nature and extent of the contingent liabilities of the company being sold, the problematic contracts it has subscribed to, the risk of litigation, intellectual property issues, labour issues and many more. In other words, the company is studied from top to bottom, in order to expose its weaknesses.

The strategic private equity buyers often follow strict Due Diligence procedures. This involves multiple teams, employees and consultants of the buyer carrying out an intensive and thorough investigation of the company being sold.

3.1 Data Room

To make the Due Diligence process more efficient, the seller and the buyer should create an online data room. An online data room is an electronic store of key company documents. This virtual data room contains (or should contain) all-important company documents, including corporate documents, contracts (of any nature, i.e., from a partner agreement, to leases, guarantees, senior management contracts, financing, licensing, insurance, trademarks, patents, ongoing litigation or claims involving any risk, etc.).

The data room allows the selling company to provide valuable information in a controlled way, whilst also maintaining confidentiality. It helps to accelerate the M&A process by avoiding the need to have the buyer’s advisors in the company day after day, further altering the business of the seller’s company.

3.2 A Virtual Data Room

It is important to highlight that access controls can be established in a virtual data room. For example, access can be permitted to all documents or only to a subset of documents (which may vary over time), to a wide group of advisers or to a pre-selected restricted group.

This virtual system includes a feature that allows the seller to see who has been in the data room, how often and the dates of entry. This information can be very useful to sellers as an indication of the level of interest of each potential buyer and helps the seller understand what is most important to each buyer.

The companies that sell should know that uploading a lot of information to the Cloud of a data room will take a lot of time and will require significant resources from the company (both in employees, and in using employees to do the tasks of uploading, searching, etc.).

In this process, the buyer’s M&A advisor will require the seller to have all the information and documents that buyers expect to see in that data room. It’s what we call The Checklist.

3.3 The Checklist and the Data Room

The selling company should not allow access to the data room until virtually all the information has been uploaded, unless it is clearly understood that the buyer is initially granted access to only a subset of documents.

If the selling company allows access before all documents have been included and adds documents continuously, potential buyers may become sceptical about whether the seller has fully disclosed all the information and documents that buyers consider important. This scepticism could impair the seller’s ability to get the best offer from potential buyers.

3.4 The Importance of Data Rooms and Virtual Data Rooms

The selling company must ensure that its books, records and contracts can withstand Due Diligence’s robust investigation of a buyer. Here are some issues that may arise:

- There is no record book of partners or registered shares.

- The proceedings or decisions of the Administrative Body are missing (or not signed.)

- The proceedings or decisions of the General Meeting of Partners or the Sole Partner are missing (or not signed).

- Contracts not signed by both parties.

- Contracts that have been modified but without the terms of the amendment signed.

- Proceedings of the board meetings have been referenced the same.

- Incomplete/unsigned documents related to an employee, such as stock option agreements, confidentiality agreements or patent agreements.

This process can be complicated and such shortcomings during the Due Diligence process will involve demands of the buyer, which the seller will have to rectify as a precondition for closing.

Avoid these problems by making your own “Due Diligence” before the buyer does it for you.

The Financial Statements Go Far Beyond the Annual Accounts

With regard to this question, the buyer shall demand that the financial statements of the selling company are prepared in accordance with the approved accounting principles and are consistently applied. Additionally, that the selling company fairly present the results of transactions, financial statements and cash flow over a certain period of time.

The buyer will take care of all historical financial statements of the selling company and related financial metrics, as well as the predicted results of the business in question. What may really worry the buyer will be:

- Do the financial statements and related notes reflect all the liabilities of the selling company, both current and contingent?

- Are business profit margins growing or deteriorating?

- What will need to be done in order to continue operating the business?

- What capital expenditures and other investments will be needed to continue to grow the business?

- Are the financial statements audited and, if so, for how long?

- What do the seller’s annual, quarterly and monthly financial statements reveal about its performance and financial condition?

- Are the projections for the future and the underlying assumptions reasonable and credible?

- How do the projections for the current year compare to the board-approved budget for the same period?

- How is “working capital” determined for the purposes of the procurement contract? (defining differences can result in a large variation in the final price of the trade.)

- What are the selling company’s current capital commitments?

- What are the statuses of the assets? What levies are there?

- Are there unusual revenue recognition issues for the selling company or industry in which it operates?

- Does the seller have sufficient financial resources to continue trading in the ordinary course and cover its transaction costs between Due Diligence and the expected closing date of the acquisition?

- What debt is outstanding or guaranteed by the selling company, what are its terms and when shall it paid?

- Are there problems with accounts receivable?

- Are the capital and business budgets correct, or have the necessary capital expenditure been deferred?

- Should a report on “income quality” be commissioned?

- Have EBITDA and adjustments to EBITDA been calculated correctly? (This is particularly important if the buyer is obtaining debt financing)

- What warranty responsibilities does the selling company have?

The More Interest = The Better Position for the Seller

The seller usually gets a higher bid when there is more interest in the company.

The process becomes more competitive and can lead to a price increase or better selling conditions, or both.

Negotiating with a singular buyer (knowing that there is only one buyer) will put the seller at a clear disadvantage, particularly if the seller agrees to an exclusivity agreement that limits their ability to enter into negotiations with other potential buyers for a certain period of time.

The Price is Always Negotiable

How do you know if the purchase price is equal to or greater than the value of the company?

It is important to understand that the offered price and valuation, like other terms of the M&A transactions, are negotiable.

However, since the company’s shares are not publicly traded, the reference point may not be as clear in advance and the outcome of this negotiation depends on a number of key factors, including the following:

- Whether there are multiple buyers for the company or a single interested party.

- The company’s projected financial growth.

- Comparable in the market (are the competitors selling multiple ‘x’ which is equivalent to ‘n’ times their income? Or 12 times larger than the EBITDA?) Is the company growing faster than the competition?

- Business, financial or legal risks that the company face.

- If the buyer is a financial investor (such as a private equity firm that can value the company based on a multiple of its EBITDA) or a strategic buyer (who can pay a higher price due to synergies and strategic adjustment).

- The company’s prospects and opportunity for series funding rounds.

- The experience and knowledge of the management team.

- Take as reference the prices paid in the last sales to employees or investors in the early stages of the company.

- The patented technology of the company or of which the company is the licensee of.

- The report carried out in the company’s last round of financing.

- The company’s business sector.

- Trends in the company’s historical financial performance.

- If the seller and the potential buyer cannot agree on the purchase price, consider an ‘earn-out’ as a way to compromise on the difference in price.

- An ‘earn-out’ is a contractual provision in the purchase agreement that allows the seller to receive additional and future performance if the business achieves certain financial metrics, such as achieving certain gross income or a certain EBITDA.

- While an earn-out may pose significant risks to the selling company (and its shareholders), it also paves the way for selling shareholders as with the sale of the company, they can achieve their return, which is based on the development of the sold company after the transaction closes.

- Finally, don’t be afraid to negotiate. Even if a number proposed by a buyer seems to you to be “right,” consider making a counter-offer. Buyers rarely make their best offers at the start. As good negotiators, buyers keep an ace up their sleeve, leaving a sufficient additional fund for the for the final “concessions” before closing the deal. Therefore, a reasonable counter-offer on the price is normally not unwelcome. If you never ask, you will never know.

Good Legal Advice is Essential

It is vitally important for the success of the M&A process that the selling company hires an advisor who is specialized in these transactions. The legal team should include not only lawyers who are experts in mergers and acquisitions, but also experts in the relevant areas of expertise (fiscal, real estate, intellectual property, new technology, data protection, jurisdiction, administrative etc.).

The M&A transactions involve complex agreements with varying legal disciplines which require using complicated strategies.

To be effective, an M&A lawyer must be closely familiar with the company’s business and with the process of an M&A deal.

They must be proficient in the rules of law, be a competent advisor and negotiator and have experience in terms of contract preparation. The lawyer must have “gone through the process” many times as it is very difficult to be effective as an “occasional M&A lawyer.”

The same goes for legal specialists that are essential in the M&A transactions. Each specialist should be immersed in the legal considerations of M&A, particularly those relevant to their trade and work full time.

While it is tempting to resist hiring a “solvent” legal team for the few minutes they generate, an experienced team will actually save you money by identifying significant risks at the beginning of the deal and developing practical solutions accordingly.

In addition, a team specialized in M&A that has worked together frequently is likely to more efficient than a couple of lawyer claiming to be experts in more than one legal area, a critical issue for a M&A deal.

Consultancy on Finance and Corporate Finance

In many situations, private equity can bring significant value to the deal by doing the following:

- Help prepare the management’s presentation materials for meetings with buyers and prepare the management team in advance to assist the seller and their legal advisor in the design and execution for a perfect deal.

- Identification and contact with prospective buyers.

- Organisation of meetings with prospective buyers.

- Help prepare an executive summary or memorandum of confidential information for potential buyers.

- Work with the management team for presentations that are in front of the company’s Board of Directors.

- Preparation and organization of the signature for the confidentiality agreements or the NDAs (Non-Disclosure Agreement).

- Help the seller to upload the company’s information to the data room or virtual data room.

- Organization of the seller’s responses to requests made in the buyer’s legal review.

- Assistance in price negotiations and other key terms of the transaction.

- Advice on comparable market valuations.

- Sharing an independent opinion (recommended, especially in situations where managers have conflicting interests).

A key trait of a good financial advisor or corporate finance expert is independence, someone who knows how to lead the deal and acts as a true partner for the CEO, shareholders and management team of the company.

Do not underestimate Intellectual and Industrial Property

The seller will have to pay special attention to this area if their business develops intellectual and/or industrial property. Key issues for an Intellectual Property (IP) buyer in an M&A transaction typically include the following:

- For the buyer’s Due Diligence, the seller must have prepared an exhaustive list of all intellectual property (and related documentation) that is important to the company.

- The buyer will want to confirm that the value of the selling company, particularly if the seller is a technology company, is supported by the extent to which the seller owns (or has the right to use) all the intellectual property that is fundamental for its current and predicted activity. One area of particular importance is the extent to which all employees and consultants involved in the development of the seller’s technology have signed agreements to release their inventions to the seller.

- Many engineers and software developers use an open source code or incorporate such software into their work when developing products or technology. But the use or incorporation of such open source software by a seller’s company may result in ownership, licensing and compliance issues for the buyer. As a result, sellers need to identify and assess the problems of open source coding at the beginning of the negotiation process.

The statements and warranties on intellectual property in an acquisition serve two important purposes:

- If the buyer learns that the intellectual property statements and warrantees were false when the deal is closing, the buyer may not be required to close the acquisition.

- If the intellectual property statements and warranties are false at the time of the transaction, the buyer may be entitled to be compensated upon closing for any damages arising from the misrepresentation by the seller. Consequently, the seller will negotiate the limitations on the scope of the statements and warranties, confining the potential risk to a part of the purchase price (as little as possible). However, given the importance of intellectual property for the buyer, the buyer may apply for the right to claim up to the total purchase price if the statements and warranties of the intellectual property turn out to be false.

In general, the buyer wants the seller to declare and guarantee that:

- The activity of the selling company does not infringe, embezzle or violate the intellectual property rights of any other party (or of a third party);

- No other part of the selling company is infringing, embezzling or violating the intellectual property rights; and

- There are no litigation or complaints about these matters (above) that are pending or threatened. These statements and guarantees are extremely important to a buyer because a post-closing lawsuit which claims an infringement not known prior to closing may expose the selling company or the buyer to substantial damages or, worse, the loss of the right to use the intellectual property it acquired. Of course, a seller does not want, and should not, assume the entire risk of infringement. That said, the extent and limitations of the statements and guarantees are negotiated and the outcome depends on the power and negotiating capacity of each party.

The buyer will be concerned about the excessive breadth of licensing and the change of control – corporate or administration – in the agreements related to the intellectual property of the selling company. For example, if a key licence ends with a change of control, the buyer may seek a substantial reduction in the price or abandon the deal altogether. A cautious seller will review the intellectual property documents at the beginning of the negotiation process to identify these provisions and work with the advisors to develop a strategy to address any identified risks.

The buyer will carry out a careful examination of the selling company’s participation in any current or past intellectual property litigation.

The buyer will want to confirm that the seller has implemented and maintains suitable policies, practices and security and especially in relation to data protection and privacy. With recent highly publicised data breaches and significant changes in applicable laws (such as the new European Data Protection Law) buyers are particularly aware of cybersecurity and data privacy issues within the acquisition process. Furthermore, sellers should anticipate these concerns and carry out a thorough review of their policies, practices and security, as well as possible exposures and non-compliance with legal requirements. This will allow the selling company to effectively negotiate the provisions of the procurement agreement, related to cybersecurity and data privacy.

The Contract of Sale

The acquisition process concludes with a sales contract whose wording protects the seller as much as possible. The buyer’s lawyer is the one who usually writes the contract of sale, so it is vital that seller’s lawyer knows how to negotiate the terms so that their client does not give more than necessary.

10.1 Key Provisions of a Sales Contract:

- The structure of the transaction (for example, purchase of shares, purchase of fixed assets or merger.)

- The purchase price and related financial terms (how much savings should the company at the time of closing so that it can continue to operate, what dividends can be distributed beforehand by the selling partners, etc.).

- Possible price adjustments (ideally, the seller wants to avoid lowering the price but if so, the reduction is to be based on calculations of working capital, employee issues, etc.).

- Milestones or other triggers of earn-out payments or contingent purchase price.

- Amount of the deferred price or of the deposit given in guarantee for potential claims that may arise after closing and for the buyer, a period of the guarantee or retention deposit (an attractive scenario for a seller does not exceed 5-10% of the purchase price with a guarantee deposit period of 9 to 12 months but know that these transactions usually set an average term of 12 to 24 months, in the worst case 4 years or statutes of limitations).

- The exclusive nature of the escrow/ holdback for noncompliance of the sales agreement (except perhaps for beaches of certain fundamental statements).

- The conditions for closing (ideally, the seller wants to limit the conditions to ensure that they can close the transaction quickly and without the risk of unfulfilled conditions).

- The nature and extent of the statements and guarantees (a seller wants them to be assessed as far as possible by materiality and knowledge experts).

- If the closing of the deal does not take place immediately after the signature, it is vital to have regulated the actions of the seller in terms of business management, what happens with the commercial agreements that arise between signing and closing, what sort of acts must be previously communicated to the buyer, whether or not they are able to close contracts, etc.

- The extent and exclusions of compensation.

- The treatment of employee share options.

- The conditions of employment of any management team/ employee by the buyer.

- Provisions for the termination of the sale contract.

- The responsibility and cost of obtaining any consent and approval regarding competition, money laundering, regulatory authorities.

Conclusion:

The process of selling a company or an acquisition involves much more than agreeing on a price. There are several hundred aspects to negotiate. And if one refuses to agree on a price or sell their company, they won’t be able to buy someone else’s company. It is not about charging fees. This is simply business. Even if one certain company does not buy the selling company, it will be bought one way or another.

Essential breach and breach with resolutory significance

Penalty clause and its moderation in Courts

")